While this company makes you look through the mist of the dark

Mr Mimetic tries to look into the future

It’s good to have friends. It’s even better to have smart friends with opinions. The company we are about to explore is a hat tip from a friend who runs a family hedge fund, with all of his own capital invested.

Mr Mimetic received this text on WhatsApp:

Ye should hae a keek at … *

Usually, that should be enough to get Mr Mimetic really curious. But busy-busy times are upon us, so Mr Mimetic neglected the call to action. Yet, Mr Mimetic’s friend wouldn’t have it. Three times he urged to take a look.

We usually like to discuss what we like and what we don’t like about a stock.

Mind you, his investing philosophy is quite different from Mr Mimetic’s personal portfolio and the philosophy of this experiment: the Mr Mimetic Fox Fund.

This makes us a great “red team” for each other. Only once in a while, we own the same stocks.

Then, he mentioned he dove in and took a position.

So, let’s take a look, shall we? Could this be one of those rare instances where we take the plunge together?

The price is wrong

First of: let’s play a guessing game. Mr Mimetic gives you the numbers, and you can take a guess at the market cap, or the valuation metric.

What would you pay for this kinda business? What do you think is a reasonable price?

This is from the press release on October 14th, 2024:

The Balance Sheet is clean. Enterprise Value is lower than the Market Cap, so there is net cash.

Some extra data points, to be able to guess the price:

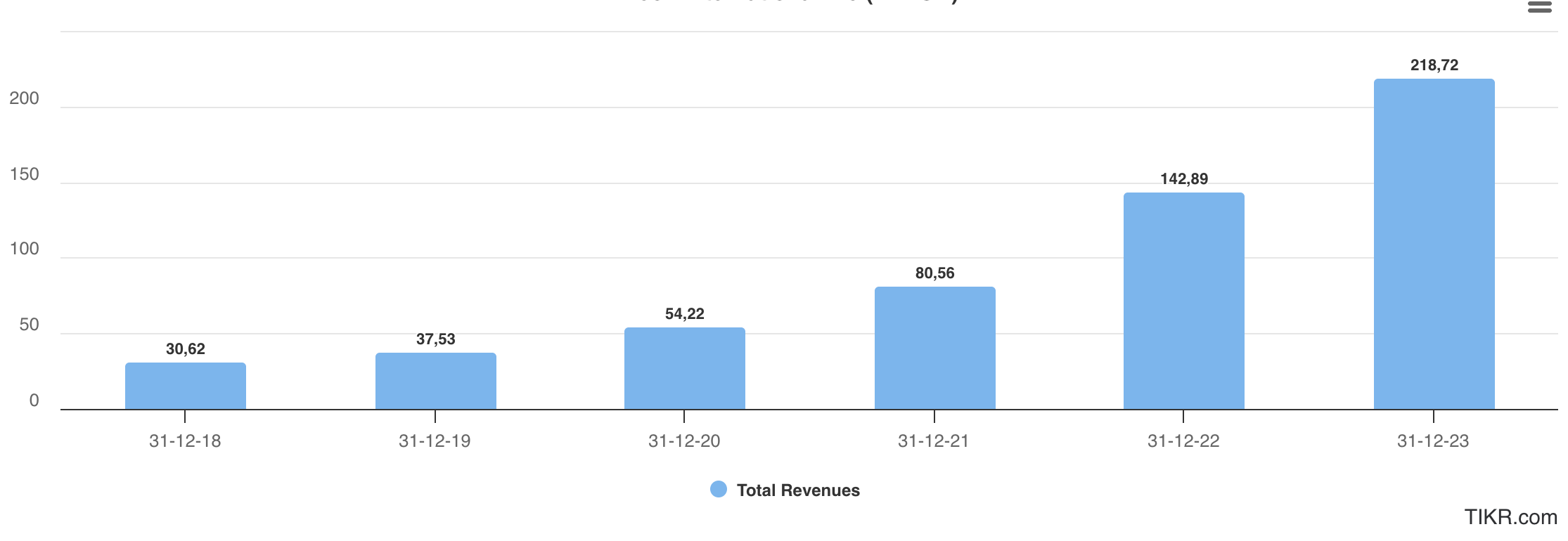

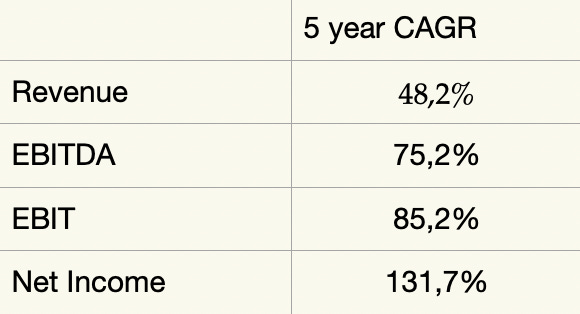

Indeed, the last couple of years have shown:

stellar revenue growth

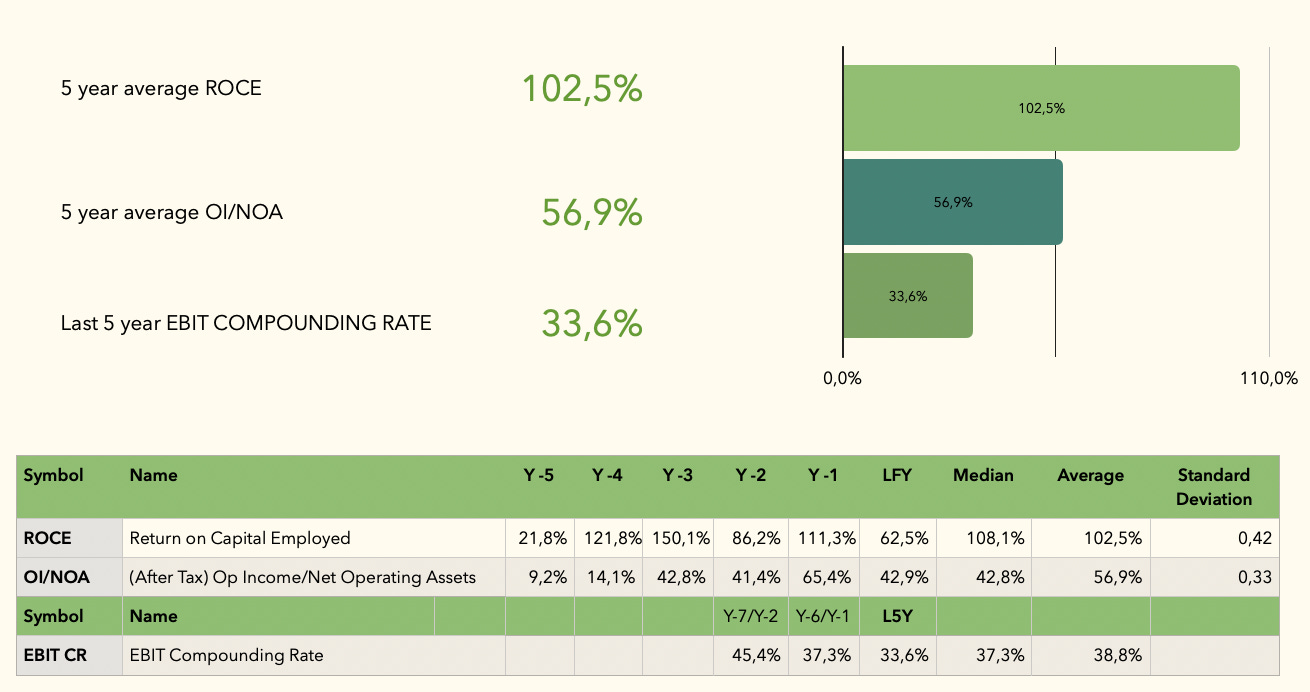

great Return-on-Investment numbers

rather good Compounding Rates

“Compounding Rate” refers to this quote by Buffett:

“The best business to own is one that over an extended period can employ large amounts of incremental capital at very high rates of return.” - In: the 1992 Berkshire Hathaway Shareholder Letter

It’s about how fruitfully you can re-invest the profits you make in new business-lines. Your ability to incrementally grow revenue, and grow those extra profits at attractive rates of return.

When Free Cash Flow is calculated, investments in new businesses are deducted, so a lower Free Cash Flow number is expected in companies which invest heavily in the future.

“Free cash flow is a perverse valuation attribute, for firms reduce free cash flow when they invest to add value”

- professor Stephen Penman, in: On Comparing Cash Flow and Accrual Accounting Models For Use In Equity Valuation

Mr Mimetic came to the conclusion that it is a better strategy to combine high Returns-on-Capital-Employed and Returns on Net Operating Assets, with high Compounding Rates.

The biggest argument to do so, is: why not?

Both are signs of high quality, so why not set the bar really high since we want to maximize our returns going forward.

Anecdotal evidence suggest this is a golden combination that might be predictive for above average returns.

We are patient. We have no restrictions in terms of geography, nor industry. We have 40.000 stocks to choose from. Thus: we only have to avoid the 39600 companies that will NOT be part of the best performing 1% stocks over the next 5 years, to achieve our goal.

The counterargument would be that high returns of any kind reverse to the mean, because of expected increasing competition down the line.

As such, high returns and margins invite competition and makes your future growth more vulnerable.

So, it is quite dandy to find companies with high margins and high returns, especially on “incremental capital”, but it’s not as funky as you might think.

The main thing is to be able to predict how sustainable those margins and returns are. How good are they in fending of the competition? How sure are you that in the future they will keep that edge? And will be able to re-invest the hard-earned profits Ad Infinitum?

Again, it becomes an art.

Now, what about the price?

What would you guess the market cap is? With those numbers?

Well, it is cheap.

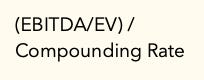

As a sort of PEG-equivalent, Mr Mimetic likes to compare the EV/EBITDA metric versus the Compounding Rate.

For this score to become 0,5 - which is the upper bound of where Mr Mimetic considers anything cheap - the EV/EBITDA multiple in this case is still… 15.

When those growth numbers are sustainable, EV/EBITDA of 15 would indeed be very cheap.

However, the reality provides us with a nice surprise:

How come?

Why is it this cheap?

There was an IPO, and the share price has suffered:

A few reasons for that:

The CEO owns a little over 70% of the company. He’s also 64 years old.

Only like 20% of the company is public

There seem to be a post-IPO seller

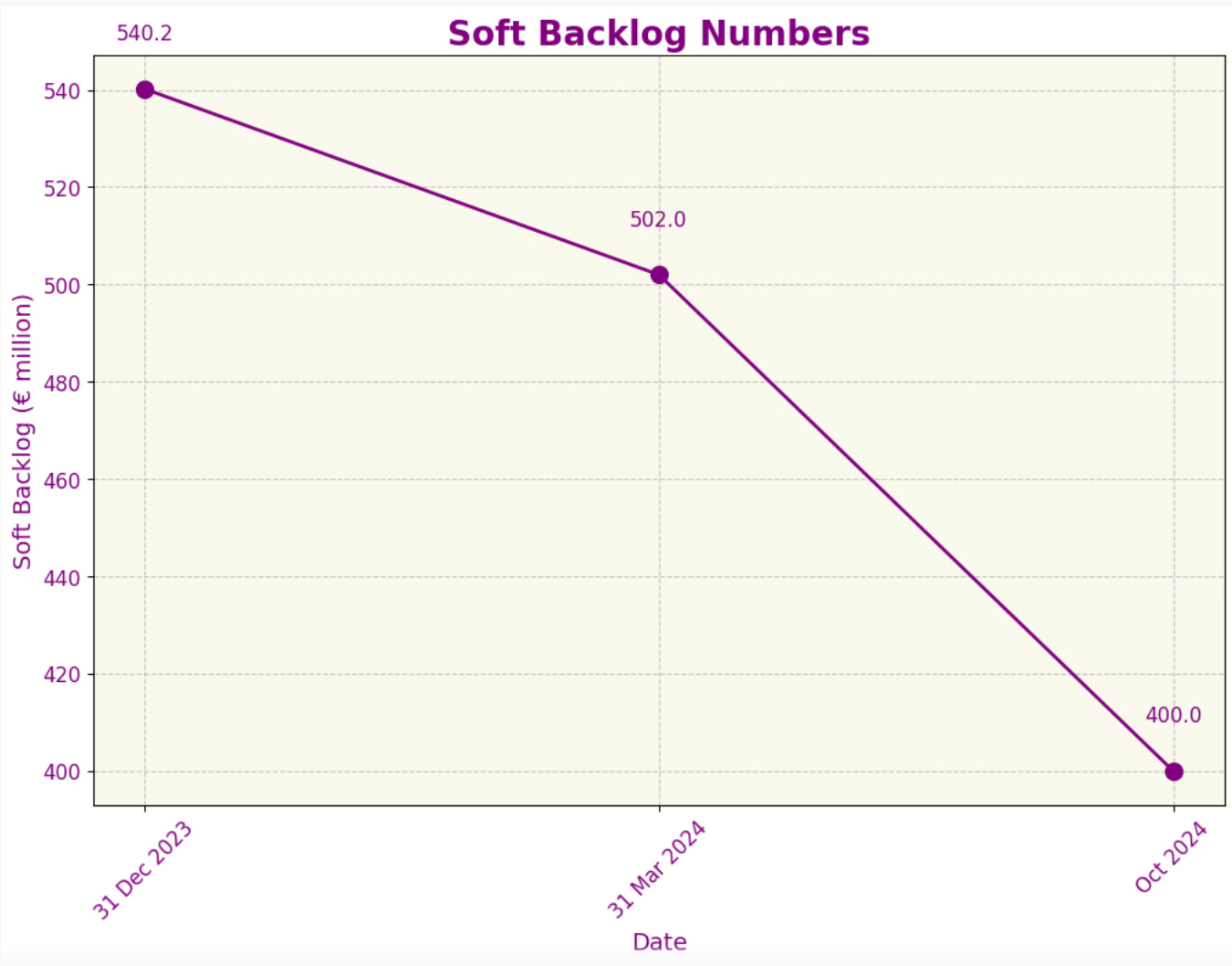

The “soft backlog”, which predicts future revenues, is trending down.

They announced that from now one there will be a dividend with a 30% à 40% payout ratio.

That being said, only yesterday they confirmed their 2024 revenue guidance to be in the €330-350 million range, plus confidence for 2025:

The anticipated order intake provides comfort that the company will maintain its growth trajectory in 2025 and repeat double-digit growth. in: Press Release October 2024

Mind you, 2023 revenue was sub-220 million.

Growth has been quite extraordinary the last couple of quarters, and that fact is totally not incorporated in the share price as of today.

Is this, indeed, a case where the selling was “indiscriminate”, and we can feel like a stock market genius?

Check, check, check

Now, when we consider all this info, we already have quite some boxes to tick on our Investing Check List:

As always, the most important and hardest questions still need to be answered.

Acquisitions

From the FAQ on the website:

The main drivers of our growth strategy are: growing in currently underpenetrated geographical locations, such as in Asia; becoming increasingly vertically integrated; ensuring efforts are focused on product innovation into adjacent products, such as platform-based products, in order to fulfil a greater proportion of customer needs. In addition, we aim to explore strategic M&A opportunities to acquire companies in both our core and adjacent markets.

Also in the FAQ: “What is the primary focus of your M&A activity?”

We have a good pipeline of partnerships and M&A opportunities, including vertical integration opportunities, which solidify our supply chain and increase our certainty over component supply.

Especially, the 100 million capital from the IPO will be used to do acquisitions.

In September, they announced a majority stake in a German firm who is a niche supplier, for 34 million € (which is about 2x revenue and mid-single EV/EBITDA).

This seems like a good strategy since you know your supplier’s worth, from day-to-day interactions. The margin of error should be smaller.

Obviously, when you are a big client with a critical supplier, you have a lot of leverage to “push” for an acquisition. In the end it comes down to selling to you, or loosing you as a client…

Also, they have communicated they payed 23 million for the equity in the company (the other 11 million is cash for investment in growth), while “as a comparison, more than EUR50 million to realize a greenfield investment in this industry.”

They are confident they can triple sales in 5 years time, in part because…

“(Our) brand name and supervision is going to have a premium effect on the price,” - H1 20224 Conference Call

In reality, we have not enough information to assess how good they are handling acquisitions and if it will result in adequate returns.

So the jury is still out on that one. But Mr Mimetic is optimistic. It does seem like a smart strategy.

Apart from that, they did announce that before year-end, there will be more acquisitions:

“We have been working very diligently the last six or seven months in this front. And we believe we will be able to announce something before year-end.” - the CEO

Margin Expansion

This one is also quick and dirty to review.

Ideally, you want to see a Margin Expansion: with every extra dollar sold, you want to see more cents drop to the bottom line.

This is not apparently the case:

Case in point: this is a hardware company, with only some software and services included in the product offering.

Industry

So, what do they sell exactly? What do they make?

This:

Night vision and thermal imaging.

In most of their core market they have like a 50% share, with other companies mostly occupying their niche, or delivering non-specialized Nigh Vision Goggles as part of larger contracts.

Obviously, the main clients are military, intelligence departments and security firms.

And those are not won over easily.

Consistency is important: you want top notch performance every second of every mission. You can never let your users down. Their lives are at stake.

So, Mr Mimetic does consider the industry one with high barriers to enter.

Because of the combination of expertise, proprietary technology and relationships.

For your interest: the industry is projected to grow around 11% as a whole the coming years.

Addressable Market

As shown in the “acquisition” part they still have a lot of ground to cover in Asia and North America. They chose to start joint-ventures with local partners with longer standing relationships to penetrate those markets. As subcontracters, for the US Marines, for example.

Also, acquisitions in new territories to land and expand are on the menu.

They have bids outstanding for over 500 million in revenue. Not all those bids will be won, of course.

The market is now about 4 billion ; so we can say that this company has a world wide 10% market share.

As the market expands due to renewed urgency in military spending worldwide, the projected market size in 2032 is about 8 billion US$ market for military grade devices.

NATO countries collectively have approximately 3 million ground forces personnel, highlighting significant potential for continued expansion. - Jan from Lowbill Research

The expectation is that more and more of those ground troops will be equiped with Night Vision, on a 1-on-1 ratio.

There are of course potential retail applications (like night or thermal vision on your phone) that provide possibilities, maybe through acquisitions.

Now, to be able to reach 10x from where we are right now, the following questions need a positive answer:

can they increase their market share?

can the price multiple expand?

A growth in market share, in an expanding market is possible - albeit a lot more moderate than the previous years.

“Ye should expect 15-20% growth…if ye apply that to EBITDA, it’s currently valued at 5 times 2026 EBITDA” - Mr Mimetic’s hedge fund friend

If the market doubles (as projected), and they can grow towards a market share of 15% instead of 10% now, we are looking at 1.2 billion in revenue.

As said, Mr Mimitec considers a 15 EV/EBITDA still as cheap (all things considered equal), which translates in roughly 3,75 in EV/revenue.

That would amount to a market cap of 4,5 billion vs 644 million right now. That’s a 7-fold.

Everybody would be happy with that.

But we can all agree this is like a really smooth scenario, where a lot of things have to go just about right.

With a tight float as it is now, high multiples will not easily happen.

“For me, the issue is more the limited free float. 70% is in the hands of the founder who is 63 years old” - again, said friend

The CEO did suggest they might venture into “fire control systems”, since there is a huge increasing demand in that area.

So, what to do?

What is their position in the market?

Are they mission-critical? Do they have a proposition that is hard to deny?

What is their edge? What makes them unique?

Competitive Advantage

A Night Vision Goggle is not just a Night Vision Goggle. It is bespoke. Each army, regiment, or task force has different requirements. They proud themselves that they are very agile to meet the very specific needs of their different customers:

“Deliveries are always customized to ensure that the NVGs integrate seamlessly with soldier systems, various platforms, and any specific operational requirements” - Jan from Lowbill Research

This is indeed different from some of the bigger defense contractors who also offer Night Vission Goggles, without many specifications, alternations, or client-specific adjustments.

It seems like they are at the cutting edge of innovation:

It’s like a Google glass for soldiers: vital information such as friend-or-foe identification and geo-location details are displayed directly within the user’s field of view. The Group has already secured its first orders - Jan from Lowbill Research

But that is something you would expect.

A tangible advantage is the European based supply chain, that will be more and more vertically integrated, as time passes and acquisitions are tucked in:

high investments into securing parts of their supply chain, resulting in a capital light business - Jan from Lowbill Research

(they did a small acquisition in South-Korea, to be able to have a local supply chain in Asia)

This results in significant higher margins and returns than the competition:

Return on Invested Capital (ROIC), (…) is significantly higher than that of its peers.” - Hugo, from Undervalued and Undercovered

Now, numbers are not culture.

But culture translates into numbers in the long term.

And those numbers could very much be sustainable, because of:

“We benefit from having strong relationships with long-standing customers, which deliver a high volume of repeat purchasing to our business” - H1 2024 Earnings Call

And those high margins result in:

an extremely agile and nimble business model which enables us to operate with a competitive cost structure - the CFO

Others have summarized as follow:

a robust competitive moat, supported by long-term government contracts and a proven track record of reliable delivery - Jan from Lowbill Research

Or:

“International's strong reputation, high-demand products, extensive customer base, and experienced leadership contribute to its competitive advantages” - Hugo, from Undervalued and Undercovered

Hmm. Can we conclude: cheap, poised for growth, a strong brand and somehow “different”?

Who are we talking about?

Remember who this was?

He shares his first name with our company:

It’s a Greek company, listed on the Amsterdam exchange.

They did a challenge with Red Bull F1 Racing to have a pit stop in the dark:

Will Theon be part of the Mr Mimetic Fox Fund?

There are some things Mr Mimetic doesn’t like:

is their moat perfectly alligned with the coming expansion in military budgets or are they too specialised ; meaning the more generic military contractors are in a better position to provide mass production of entry-grade military night vision goggles?

how certain is their ability to grow substantiantial? Mr Mimetic thinks a doubling of revenue is possible in the next 5 à 7 years or so; even a tripling when acquisitions are played right, but a 10-fold seems not part of the realm of possibilites

to grow more they will have to venture in other products, like “fire control systems”. This ads opportunity, but also risk.

the float is tiny. Only a part of the company is public. The market isn’t always keen on large insider ownership stakes that just sits there.

the CEO is in the Autumn of his lifespan. Will he be able to keep the company on the cutting edge in terms of development and talent?

they are investing quite heavily in a "platform”. It’s hard to imagine how this might look like. It also seems like a step away from the core product? (if this works out though, margins should expand with growing volume)

will expansion in new markets through joint-ventures eat up the margins and compounding rates?

the newly installed dividend is an indication that the company doesn’t see enough opportunity to re-invest its capital at high enough returns. This is a red flag when we are looking for growth stocks.

“global geopolitical conflicts and emerging threats have put the supply and demand for night vision technology in a delicate balance.” - the supply chain might be interupted due global tensions…

To find out if those objections weigh heavy enough, you can upgrade your subscription to find out. (only $30/year)

If you like what you’ve read, please consider sharing this post with your investing aficionados

Kind regards,

Mr Mimetic.

* Full discosure: Mr Mimetic’s friend nor Mr Mimetic has English (nor Scottish) as our native tongue. It was an attempt to translate the dialect we speak together.

A FEW SOURCES

The 1992 Berkshire Hathaway Shareholder Letter

On Comparing Cash Flow and Accrual Accounting Models For Use In Equity Valuation